Elizabeth Warren’s proposal is a good idea that progressives should support…

Senator Elizabeth Warren’s proposal to cancel a significant chunk of outstanding student loan debt sparked a backlash from higher education policy wonks. Their central objection is that the plan would be a regressive wealth transfer to high-income borrowers, who tend to have the largest outstanding balances of student debt. A better policy, so the critics argue, is to do what we’re already doing through Income-Based Repayment, but better: write down monthly obligations to the extent they’re unaffordable, and then either extend payment terms or, in the distant future, write off outstanding balances. What the Warren plan does—write off outstanding balances in the present instead—is, supposedly, beyond the pale.

This critique, that the real problem isn’t outstanding balances, but rather non-repayment, stems directly from a misunderstanding of what causes the student debt crisis in the first place. The reason why there’s a crisis of student debt non-repayment is that increasing the overall student debt load of entering cohorts did not have the effect of increasing labor market earnings. People thought that more debt would mean more education and therefore higher earnings. But instead, the labor market credentialized, reducing the earnings associated with any given level of attainment. So people needed to take on more debt to get more degrees just to get the same jobs earning the same wages. I spoke to some of these concerns in my 2018 Roosevelt Institute paper with Julie Margetta Morgan, “The Student Debt Crisis, Labor Market Credentialization, and Racial Inequality.” Here, however, I want to address the central question: Is cancelling student debt, as Senator Warren has proposed, regressive? The answer is no. But it’s important to know why the answer to that question matters a great deal for the future politics of higher education and student debt policy.

Before addressing the specifics of the distributive impact of debt cancellation, it helps to set the policy scene. Higher education experts, for a long time, denigrated the idea that the increasing level of outstanding student debt is a policy problem at all. Then they said that yes, perhaps it is a problem for the small share of borrowers who are actually delinquent on their debt, but for the vast majority who are current (including who are enrolled in income-based repayment schemes for deferring payments), student debt “pays off” because it causes workers to earn more than they would have otherwise. A variant of this theory concerns the distributional impact of student debt: Because people with more of it earn more, the story to date has been that cancelling it disproportionately benefits higher-income borrowers. The idea that student debt causes borrowers to earn more, by increasing their educational attainment and therefore their earnings, is baked into the idea that cancellation of student debt would be a regressive policy—people with the most debt need the least help, but they’d get the most money from forgiveness.

Indeed, some concluded that forgiveness would be regressive before the Warren proposal was actually analyzed. For example, the Urban Institute put out an analysis of the distributional impact of debt cancellation in 2018, one that was repeated by David Leonhardt in the New York Times. But, it turned out, that analysis contained an error that over-estimated the share of debt held by the highest earners. When pointed out, the Urban Institute researchers corrected the error and explained how they made it, but they did not change their analysis of the underlying policy proposal in any way.

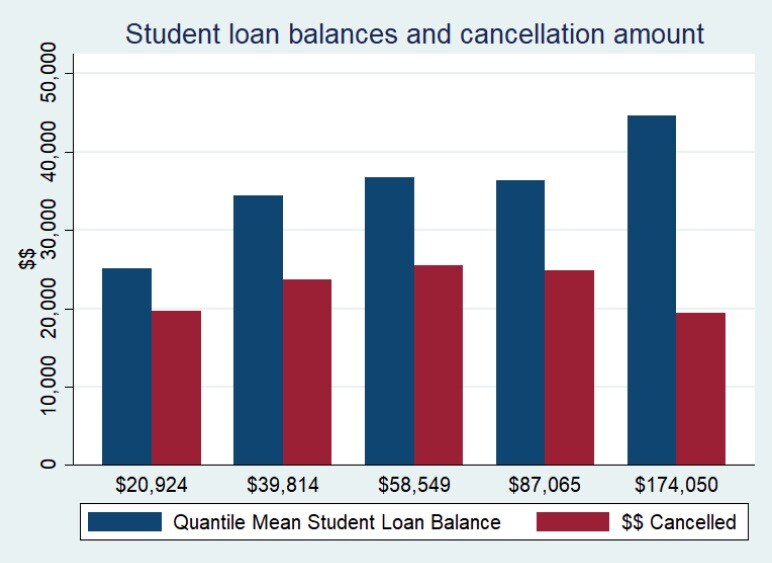

Rather than espousing policy conclusions that don’t change depending on the underlying empirical analysis, it might be useful to actually analyze the distributional impact of Senator Warren’s debt cancellation proposal. Using the Survey of Consumer Finances for 2016, I estimate student debt outstanding by income quantile among households whose head is between the ages of 25 and 40, who had a positive student debt balance, and who earned income greater than $1,000. Each of these restrictions is debatable, but it makes sense to focus on a single age cohort, since each active cohort’s experience with student debt is vastly different given that the enormous expansion of the federal student loan program is a phenomenon that occurred within the last two decades, and particularly post-financial-crisis. Focusing on only those people who have student debt elides the fact that the number of people with student debt now is a great deal larger now than it was for prior cohorts. And the growing share of the population with student debt (and especially who those additional borrowers are) tells us a great deal about why student debt has become a crisis, namely that more people need to come into contact with higher education in order to get a decent job. As tuition increases and state support decreases, coming into contact with higher education means that you need to take on student debt. But the restriction to only households with student debt matters less in evaluating the cancellation policy with respect to a single survey taken at a point in time. Finally, leaving out people with little or no income hopefully excludes people in that age cohort who remain in education full time, though of course that is not the only reason why people may not be earning.

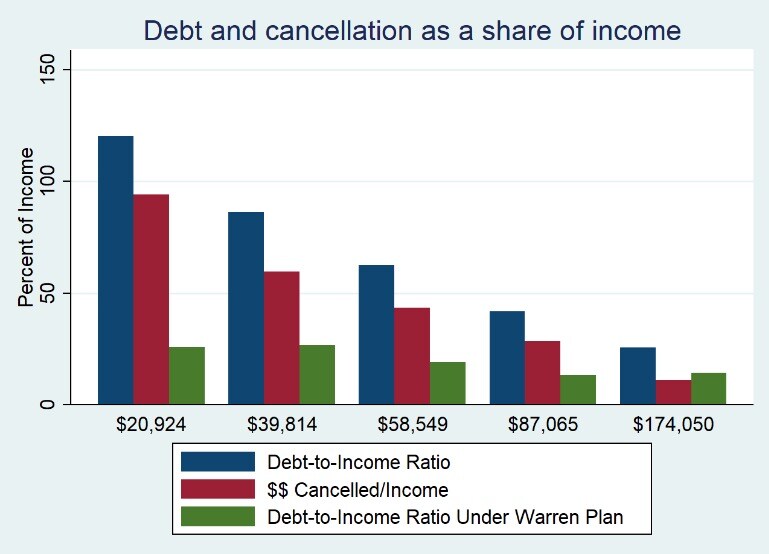

The following two charts depict the effect of implementing the Warren student debt cancellation plan for the borrowers described above by income quintile. In each case, the labels on the horizontal axis show the average income of households in that quintile. The first chart shows pre-forgiveness outstanding student debt as a dollar amount as well as the average dollar amount of debt cancelled in that income quintile. The second chart shows pre- and post-forgiveness outstanding debt as a share of annual income, as well as the amount cancelled expressed as a share of annual income.

The claim that the Warren student debt cancellation plan is regressive rests on the observation that the red bars in the first graph are increasing with income—although thanks to the limits the Warren plan puts in place, reducing the cancellation amounts for people earning more than $100,000, that amount is in fact declining for the top quintile.

But the more important implication of these two charts is that while the total amount of outstanding debt in the population is indeed increasing as a function of income, the Warren proposal would greatly reduce the burden of student debt more for lower-income indebted households. This is especially clear in the green bars in the second chart, and the fact that debt burdens decline most for the least-well-off households. Just look at those green bars. The lowest earners go from owing more debt than their annual income to owing only about ⅕ as much as their annual income. That is, the least-well-off households get the largest relative relief, and the result is a roughly constant ratio of debt levels to income across the income distribution. Compare this to the status quo, in which the poorest borrowers are by far the most burdened.

This measure of progressivity—amount of the benefit, as a share of pre-forgiveness income (or wealth)—is the standard way that distributional analysis is done when evaluating policy proposals, e.g., Tax Cuts and Jobs Act of 2017. The idea that it should be done on the basis of raw dollar amounts by quantile, as you find in the analyses that claim the plan is regressive, is not the standard approach taken in the evaluation of the distributional impact of policies.

Adam Looney, in his Brookings Institution analysis, argues that looking at cancellation dollar amounts even understates the degree to which the Warren plan is regressive. His logic is that lower-earning debtors are not making payments on their loans, or they are making lower payments than they owe thanks to the government’s income-based repayment (IBR) programs. He therefore thinks that cancellation would do them little or no good in present-income terms: Essentially, their paper debt would be erased, but they are not making payments on that debt and so they are not constrained by it.

But the fact that many borrowers with outstanding loans are not making payments on those loans, or are making payments that are lower than the full-interest-and-principal cost of carrying the loan, is not evidence that those borrowers are unburdened by their debt. Quite the opposite: It is evidence that the debt burden is so terribly onerous that it requires amelioration through another (less effective) relief policy than cancellation, namely IBR, or through delinquency or default, or taking on new debt to pay off old debt. Looney himself documented declining repayment rates for younger borrower cohorts in an important 2015 Brookings Institute paper, and particularly for nontraditional borrowers in those cohorts. The implication of that very observation is that non-repayment is evidence that student debt is increasingly burdensome over time, as higher balances spreading more widely to nontraditional and less-well-off populations run up against stagnant wages and labor market credentialization. And yet in this analysis he treats non-repayment by relatively worse-off borrowers as evidence that their student debt is not burdensome, and hence that debt cancellation would be beside the point because it wouldn’t benefit the worst-off borrowers.

This is a mistaken inference that goes back to the 2014 analysis by Beth Akers and Matthew Chingos, “Is a Student Loan Crisis on the Horizon?” Akers and Chingos concluded that a crisis was not on the horizon, because the median “debt burden”—student loan payments as a share of income—had not increased even as outstanding loan amounts had gone up. But “debt burden” measured in this way is not a good metric of the actual difficulty of paying off student debt. The fact that borrowers can mitigate their actual payments in a variety of ways is not evidence that they are not burdened by them. In fact, it is probably evidence of the opposite.

All of the ways households struggle to manage their loan payments should not be taken as evidence that they are not struggling, and IBR is not a panacea for the problems student debt poses to the economy and to household economic well-being. Looney’s analysis is yet more perverse than Akers and Chingos, because the fact that poorer people are more likely to be in these programs is itself evidence that cancellation is progressive. Student debt has delayed the economic life-cycle for a rising generation of borrowers who grew up in a world where everyone needed at least some higher education, and those who started with the least had to take on the most debt. As Looney’s 2015 paper shows, the result has been deteriorating repayment rates as the population of debtors has shifted down the income distribution and become more and more comprised of racial minorities with less access to family wealth and employment opportunities through their social networks.

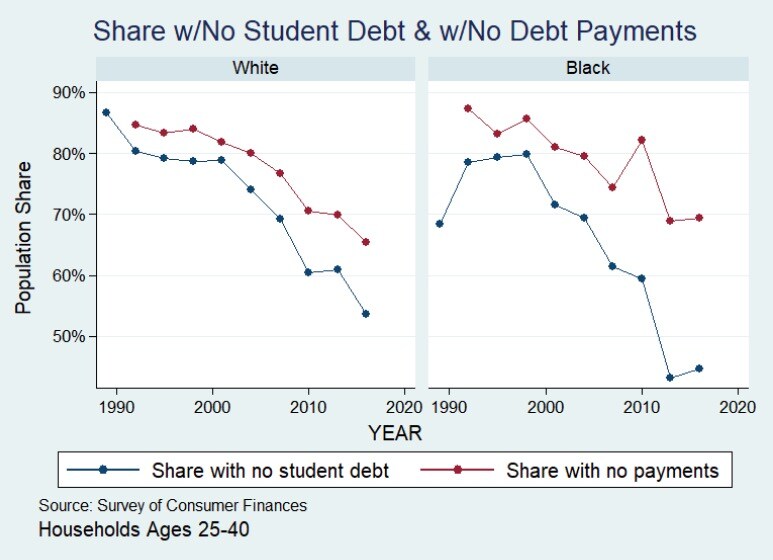

Looney rightly identifies that lower-income people make lower payments on their outstanding debt, as a share of the full cost of interest and principal repayment, than higher-income people. That is a retelling of a fact I reported in my 2018 paper on credentialization: As the share of people in the 25-40 year old age cohort without student debt has plummeted, so has the share of people who aren’t making payments on student debt—but not by nearly as much (see Figure 3). In other words, there is a growing group of people who have student debt and are not making payments on that debt in this age cohort relative to previous age cohorts. That group is disproportionately “non-traditional,” that is, from families with fewer or no college graduates, and who attended for-profit institutions.. Given the education system’s long history of discrimination and segregation, that group is, no surprise, disproportionately students of color.

To interpret this as evidence that cancelling student debt is regressive—in fact, that it’s more regressive evaluated this way than evaluating cancelled loan amounts—is a strange interpretation, and one belied by a demographic analysis of who the people are who are increasingly not paying back the student debt they feel forced to take on.

Looney also claims that many beneficiaries of a cancellation policy are undeserving because their debt derives from advanced degrees, and graduate school is either assumed to carry with it increased earning potential or, if not, that’s because the borrower made bad choices about what credential to obtain. This, too, reflects a misunderstanding of labor market credentialization, which is often the tool by which the historically marginalized and discriminated-against can navigate and ameliorate their disadvantaged position. In fact, there’s good evidence that employer power in labor markets causes workers to need to obtain more credentials. This fact may well be causing returns on all higher education credentials to decline as the overall population becomes more educated (and thus takes on more debt).

Altogether, Looney’s evaluation of the Warren plan reflects all the bad pathologies about how any amount of student debt is “good debt” that automatically pays for itself, or to the extent that it does not, it is due to poor decision-making by borrowers. This analysis has yet to take on board the many ways the vast expansion of the federal student loan program—the federal government’s most significant labor market policy of the last several decades—has failed, because it made false assumptions about how the labor market works. Senator Warren’s plan, including debt cancellation, is responsive to that more recent social science.

Looney, a former U.S. Treasury official in the Obama administration, likens the job of constructing a debt cancellation policy to loan relief for subprime mortgages during the financial crisis. He explicitly says that it was too difficult to distinguish between the deserving and undeserving and to balance that against the “cost,” presumably of spending too much federal money on those who didn’t really need a bailout. That history is in fact instructive, because it shows why Warren’s approach is so necessary. The Obama administration cared so much about the deserving/undeserving distinction and the technocratic details behind getting it right that it didn’t enact significant loan forgiveness, and in response millions of families lost their homes to foreclosure, giving rise to an economic and political backlash that may well have influenced the outcome of the 2016 election. In that case, the administration’s short-term fear of Fox News caused political second-guessing that resulted in the ultimate triumph of Fox News. Looney’s objections to the Warren plan similarly miss the forest for the trees. This is not an instance where a greater technocratic sophistication begets a more refined and better-targeted policy response. Rather, it risks seriously misdiagnosing the causes of the student debt crisis, with potentially disastrous economic and political consequences to come.

The good news in all of this is that the self-styled wonks are losing the war, at least rhetorically. In just the last few months, three progressive think tanks released overlapping sets of policy options for ameliorating the student debt crisis, which include several variations on cancellation. A few years ago, that would have been unheard of. So the political sands are shifting, but it’s a slow and painful process. Ever since I first started researching student debt in early 2015, there’s been a notable dynamic whereby the self-styled wonks lecture the masses demanding free college or debt cancellation that it’s all just too expensive, that they’re whiny millennials who just want a pony after majoring in something useless like English Literature, and that they need to pull themselves up by their bootstraps and go find a job. In reality, it’s the borrowers and the activists who know better than anyone how student debt has affected their lives, not the experts sitting in DC think tanks. That the main work of activists is to convince those deciding who gets to be admitted to “serious” policy debate about the reality of the failed expansion of the federal student loan program is perverse and frustrating, but it’s what political change demands in an era when billionaires are the ones deciding whose policy is serious and what gets consideration on the floor of Congress or in the media. The release of Senator Warren’s proposal, and the ensuing fracas among elite opinion-makers, is just another advance along that road.

Photo © Julia Lehman.

If you appreciate our work, please consider making a donation, purchasing a subscription, or supporting our podcast on Patreon. Current Affairs is not for profit and carries no outside advertising. We are an independent media institution funded entirely by subscribers and small donors, and we depend on you in order to continue to produce high-quality work.

.jpg?width=352&name=Bald_Eagle(2).jpg)

.jpg?width=352&name=Untitled%20design%20(2).jpg)