.jpg)

How do you solve the student debt crisis? This country has more than a trillion dollars of outstanding student debt, and dizzyingly high default rates among borrowers. In The American Conservative, Nick Phillips suggests that this is largely because we have failed to apply sound conservative principles. And in his “Conservative Response” to the crisis, he offers a simple plan: the federal government should charge higher interest rates to students who go to schools where they are more likely to default on their student loans. The worse your school/program, the higher your interest rates will be. That way, students will be discouraged from making bad educational choices.

Here’s how the “conservative solution” would work: the federal government would evaluate the risk of a particular degree program at a particular school, meaning it would figure out how likely students are to default on their loans coming out of that program. If a program has a high default rate and is therefore more risky for students, students entering the program would be charged high interest rates.

The assumption here is that the central problem behind the student debt crisis is that schools are getting away with providing an education that doesn’t give students their money’s worth. They’re not giving students the earning power to pay for their degrees. This is an increasingly popular way of thinking about student loans, and it can sound persuasive. In this view, students are essentially underwater on their degrees in the same way that homeowners can be underwater on their home loans. Students owe more for their degrees than the degrees are worth. The fix, then, is to incentivize students to get more economically viable degrees.

Phillips thinks the federal government is to blame for this problem because it will loan students money for any degree, whether low-value or high-value, without judgment and at the same interest rates. Schools, then, have no incentive to provide high-value degrees. No matter what the quality of the program, the feds will pay, and the students and taxpayers will be on the hook. Thus economically rational schools will keep tuition high and not concern themselves with whether they’re providing students with anything of value.

But the “conservative solution” to this incentive dilemma is to charge students more interest for going to worse schools. Yes, this is the “conservative response”: we should find the students most vulnerable, most likely to be duped by crappy for-profit schools, most likely to default on their student loans anyway, and charge them more money.

To his credit, Phillips does seem to understand some of the finer points of student debt. For instance, he notes that student debt can limit economic prospects and social mobility. He gets that maybe low homeownership rates among millennials are related to their staggering amount of student debt and not video games or phone apps or bitcoin or something. He also gets that aside from the debt itself, student borrowers can face all kinds of ancillary effects on credit and lifestyle and risk that create a sort of immobilizing web, trapping borrowers into whatever income they can find lest they risk falling behind on their student loans and getting arrested. It’s refreshing to see this viewpoint in the American Conservative, where previous student loan coverage includes a piece called “Valorizing Deadbeats.”

However, the “conservative solution” makes sense only in a kind of Econ 101 way, where you have to completely forget everything you know about the real world. In theory, students would be less likely to sign up for the higher-risk programs because they would see those high interest rates and be redirected to lower-risk schools. Phillips thinks there are three possible results from this shift in incentives: (1) schools lower their tuition in order to entice students despite the high interest rates; (2) schools make their programs better to reduce the default risk and lower the rates; or (3) high-default programs would simply close. The high interest rates would communicate to students how risky a program is and, at least theoretically, have an added benefit of offsetting costs to the taxpayers for high-default programs.

You, dear reader, may have already thought of a dozen problems with this approach. Here’s one: what prospective student looks at the interest rates in their financial aid package when deciding on a school or program? My student loans range from less than 4% interest to more than 7.5% interest, a fact which I only learned after I graduated. Was I being a responsible consumer of a financial product when enrolling in college? Obviously not. Here’s an analogy people may be more familiar with: Did high-cost loan structures stop people from taking out risky mortgages pre-recession?

It’s also worth noting that default information is already publicly available, meaning that the interest rates are supposed to signal a fact that is already easy to access. Phillips uses Cooley Law School as an example of his argument—75% of graduates don’t find work as lawyers—but that information is already available and easier to find than the interest rates on loans you would take out to go to Cooley. Would someone who is willing to spend $50k per year to go to Cooley Law School, at 7%+ interest and despite atrocious employment numbers, really change their mind at 10% interest? Maybe they would, but it’s a dangerous assumption to make without any evidence.

And that’s just thinking about law students. What about a school like the University of Phoenix? It’s a for-profit giant notorious for its fantastic marketing targeting first generation students who are looking to improve their station in life. The Department of Education publishes an easy-to-read information page on the University of Phoenix showing, for example, that California students typically graduate with more than $30k in debt, and that 73% of them aren’t able to pay back a single dollar of that debt within three years of graduation. 73%! If that fact doesn’t discourage students from enrolling, why would a higher interest rate? It seems more likely that the University of Phoenixes of the world would simply talk and sell and cajole their way around the higher interest rate with prospective students just like they do with their horrendous post-graduation repayment numbers.

The danger in Phillips’s plan falls on borrowers, of course. His proposal identifies a problem with the federal government and with schools, and then puts the burden onto borrowers who are already in a bad way. Why? Why place the risk on vulnerable students, inevitably putting many of them deeper in debt?

Why not just address the problem directly? If you want schools to lower the tuition for low-value programs, you could limit the amount of federal student aid schools can get for students attending these programs. It’s so much more direct! Then schools would have to either lower the cost of tuition or improve their programs, and students wouldn’t be at risk of falling deeper into debt. Or, if a program is so bad that everyone would be better off if it was closed, make it ineligible for federal student aid altogether. It makes more sense to directly address poor performing schools rather than putting vulnerable students at risk by trying to use market mechanisms in a broken market.

Here’s a third option: make schools pay back loans that the students can’t afford. This would incentivize schools to either provide more value or do it more cheaply. The burden would be on schools to provide something of relative worth, and not on students to read and understand differential interest rates and incorporate that understanding into the extremely difficult and intense process of choosing where to spend maybe the most formative years of their lives.

This leads to the largest problem with the conservative view—seeing higher education mainly as a financial transaction. The

“conservative solution” supposes that students should be deciding where to go to school and what to study based on the financial consequences of those choices. He points out that, under his plan, it’s possible that only wealthy students would get degrees in the humanities because they either wouldn’t need student loans or would be able to afford the high interest rates those degrees might carry. (This plays on an incorrect assumption that humanities degrees drive the student loan crisis. There’s far more evidence that the crisis thrives in vocational, career-oriented programs at for-profit colleges.) But why would those wealthy students go for low-return degrees if there wasn’t some other value at play?

The answer should be obvious to anyone who didn’t major in petroleum engineering. Higher education is as much or more about personal enrichment and exploration than it is about future financial prospects. That’s why students care about the lifestyle and culture at schools and not just graduation rates and salaries (and especially interest rates). That’s why people major in German literature and theater and pre-modern philosophy, even if they end up with completely unrelated jobs. College, for privileged and fortunate people at least, is about learning what you enjoy and what you’re good at while you also learn how to exist as an adult in the world and relate to other people. Shouldn’t that be the case for everyone? Do we really want it reduced (for poor people particularly) to how much money you will make and when you will repay your loans?

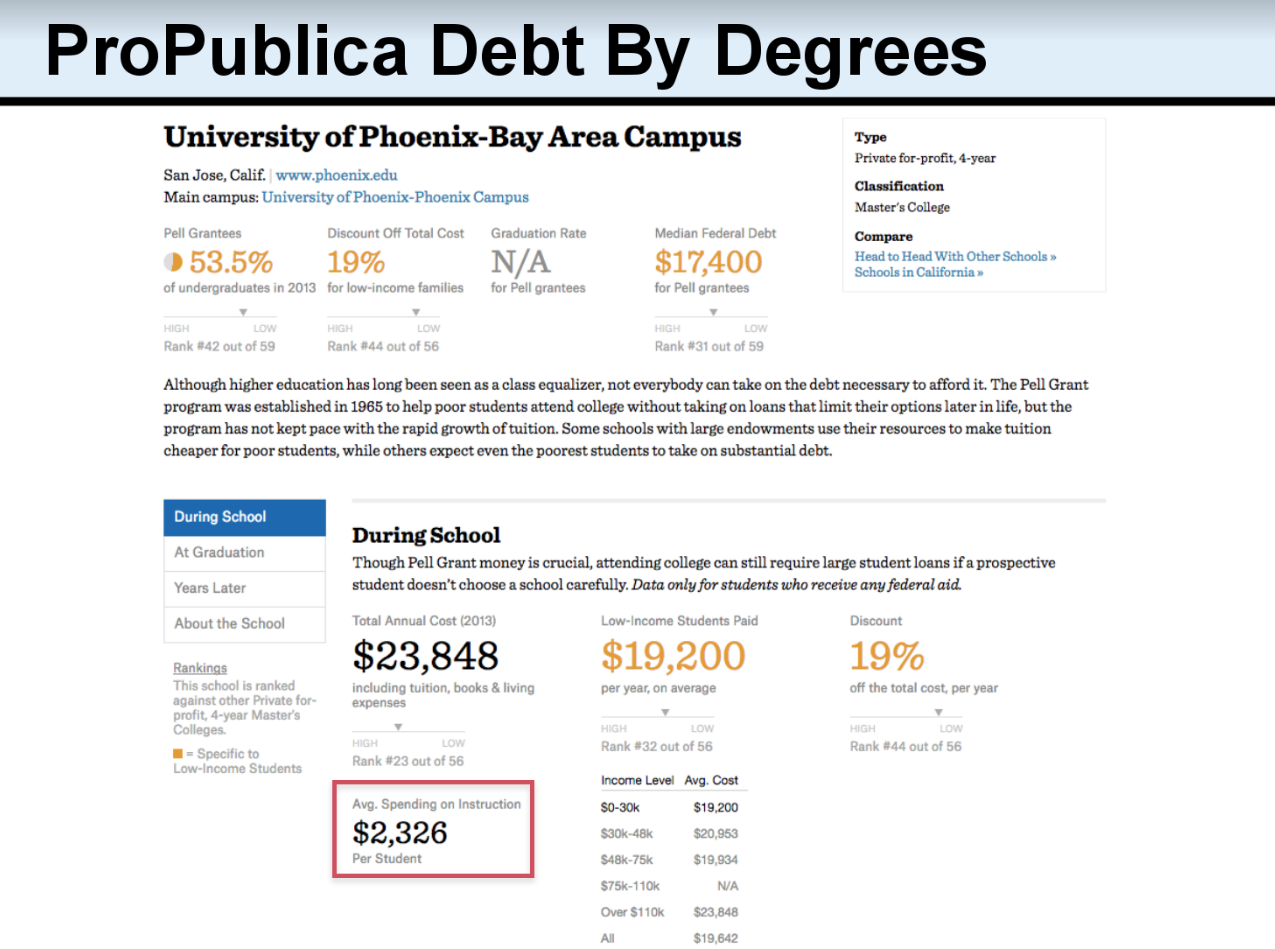

Understanding college this way explains a lot of the behavior the “conservative solution” is trying to influence. It explains why people behave in a way that free-market conservatives would see as irrational, attending high-cost programs unlikely to result in high-wage jobs. It also explains how and why low-value universities can game people’s emotions and visions of themselves to convince them to enroll, and distract them from their actual financial prospects after graduation. (Just watch these ads. Think about how much money the University of Phoenix spent producing a Pixar-quality animated minute of emotional manipulation—one that now has 11,000,000 views. Think about how these ads simultaneously play on prospective students’ feelings of inadequacy about not going to college and their pride about being a real adult with real responsibilities. Then think about the fact that of its $23,848 average annual tuition and expenses, University of Phoenix only spends $2,326 on instruction. That’s 9.7% of tuition spent on instruction per student, compared with 48.9% at a mid-range public school like CSU Los Angeles, 82% at Harvard, 124% at UCLA, and 154% at Stanford.)

Make no mistake, federal student loans are a regressive tax. People who can’t outright afford college have to pay the federal government much more over time than their richer peers have paid up front. Phillips calls for a policy change to make the system more regressive, by charging people more money who are less able to pay it back. In that way, maybe it truly is a conservative response.

UPDATE: In The American Conservative, Nick Phillips has written a rebuttal entitled “More Bad Liberal Thinking On Student Debt.” Below is our writer’s reply to the reply:

Nick Phillips cranked out a fairly thoughtful response to my critique of his student debt plan, and I’d like to thank him for it. Godspeed to him on his finals. Let me quickly address a couple of his points. First, some of the response boils down to: “Nuh-uh, students might look at interest rates, or maybe we could make them.” We can agree to disagree about whether even extremely prominent disclosures of things like APR, which most people don’t understand anyway, will ever make a difference. But Phillips also misunderstands a couple of my main points. (To be fair, I could have been more clear.) He first said that his plan would have the benefit of forcing programs to lower tuition, increase quality, or close down altogether. I pointed out that the plan accomplishes this by putting a heavier financial burden on students, and that you could accomplish the same thing more directly in a few ways. Specifically, you could do it by limiting the amount of aid that programs are eligible for, shutting them down directly, or making them cover student defaults. Phillips responds that these could have disastrous consequences. But I agree! I don’t think any of these plans is a good approach. I only meant to show that if you really want to think of education as a financial transaction where the risk of default is poorly allocated (i.e. to the students and taxpayers), you could more directly allocate it to the schools and avoid some collateral damage to students. (Phillips also worries about putting the federal government in charge of deciding which programs can be shut down. But his proposal does something similar: it’s not the market that would set the interest rates, it’s the federal government.)

My actual position here is that higher education, at least through bachelor’s degrees for now, should be free and open to everyone. I made a short case for why at the end of my article. Phillips calls the notion that college should be about self-discovery to be elitist. I agree that, right now, it is a privilege mostly only afforded to elites. But it shouldn’t be! Studying things you love because you love them shouldn’t be a luxury only afforded to the rich. If higher education were free and open, it wouldn’t be such a luxury. Sure, there would still be economic considerations in how people spend their time in college. But those considerations wouldn’t be compounded (literally!) by the federal government wielding predatory interest rates on non-dischargeable debt over only non-rich students. It’s no criticism to say that this view of college comes from a position of privilege. I agree—I acknowledged it explicitly in my piece. I just also happen to think this is a privilege that should be afforded to everyone. And I’d love to see a conservative plan for accomplishing that.

{kind=link}